By clicking "Accept all cookies", you agree to storing cookies on your device to enhance site navigation, analyze site usage and assist in our marketing efforts as outlined in our privacy policy.

By clicking 'Accept all cookies', you agree to storing cookies on your device to enhance site navigation, analyze site usage and assist in our marketing efforts as outlined in our privacy policy.

Fintech companies face a unique branding challenge: they must simultaneously signal innovation and stability. Good fintech branding agency knows it well.

Move too far toward "disruptive tech startup" and customers worry about trusting you with their money. Move too far toward "traditional financial institution" and you lose the differentiation that makes fintech compelling.

This tension defines fintech branding. You're asking people to trust you with their most sensitive information — bank accounts, investments, credit, payments — while also convincing them you're better than the institutions they've used for decades.

The stakes are enormous. A fintech brand failure isn't just a marketing problem — it's an existential threat. Loss of trust in financial services means customers leave, regulators investigate, and the business dies.

But the opportunity is equally enormous. Financial services is a massive market, and incumbents are often genuinely terrible at customer experience. Fintechs that get branding right — Stripe, Revolut, Nubank, Chime — have built brands worth billions by earning trust that traditional banks have squandered.

Case studies from fintech brands that got it right

Let's build trust at scale.

Why Fintech Branding Is Different

Revolut Fintech Branding

Financial services branding operates under dynamics that don't exist in other categories.

Money Is Emotional

People's relationship with money is deeply emotional — often more than they realize or admit.

Fear: Of losing money, of fraud, of making wrong decisions, of not having enough Shame: About debt, financial mistakes, lack of knowledge Anxiety: About the future, about bills, about financial complexity Aspiration: For security, wealth, freedom, status Distrust: Of financial institutions (earned over decades of bad behavior)

Fintech brands must navigate these emotions carefully. The wrong tone can trigger defensiveness. The wrong visual can feel frivolous with something serious. The wrong message can amplify anxiety instead of relieving it.

Traditional banks often fail here — they're so focused on appearing stable that they feel cold and intimidating. Fintechs have opportunity to be warmer and more approachable, but must do so without undermining trust.

Regulation Shapes Everything

Financial services is heavily regulated. This affects branding in ways other industries don't face:

What you can say: Marketing claims are scrutinized. "Guaranteed returns," "risk-free," and similar language can trigger regulatory action. Legal review is essential for all marketing.

How you can say it: Disclosures, disclaimers, and fine print are often required. This affects design (where does disclosure go?) and copywriting (how do you communicate clearly while satisfying legal requirements?).

Who you can target: Some financial products have suitability requirements. Marketing to wrong audiences can create compliance issues.

Where you can operate: Licensing varies by jurisdiction. Brand may need to communicate geographic limitations.

What you must disclose: APRs, fees, risks, terms — regulations mandate disclosure that affects messaging and design.

This isn't just a legal constraint — it's a branding opportunity. Companies that communicate clearly about terms, fees, and risks build trust. Regulatory compliance, done well, becomes a trust signal rather than a burden.

Security Is Table Stakes

In fintech, security isn't a feature — it's a prerequisite. Customers assume their money is protected. Any signal to the contrary is disqualifying.

Brand implications:

Visual professionalism: Designs that look amateur trigger security concerns. "If they can't make a professional website, can they protect my money?"

Trust signals: Security certifications, compliance badges, bank partnerships — these must be prominent without being the entire message.

Communication during incidents: How you communicate about security issues (breaches, outages, fraud attempts) defines brand perception. Transparency builds trust; obfuscation destroys it.

Infrastructure visibility: Some customers want to know about encryption, data handling, and security practices. Having robust security content builds confidence even if most users don't read it.

Competition Is Intense and Specific

Fintech categories are crowded and competitive:

Payments: Stripe, Square, Adyen, PayPal, and hundreds more Neobanks: Chime, Revolut, N26, Nubank, Monzo, and many regional players Lending: SoFi, Affirm, Klarna, Upstart, and countless specialists Investing: Robinhood, Wealthfront, Betterment, Public, and more Crypto: Coinbase, Kraken, Gemini, and the ever-evolving landscape Infrastructure: Plaid, Marqeta, Alloy, Unit, and many others

Differentiation is difficult because:

Features are often similar (payments is payments)

Regulations constrain what you can offer

Switching costs are low for many products

Trust is hard to build and easy to lose

Brand becomes one of the few sustainable differentiators. The company that builds the strongest brand relationship wins customer loyalty that features alone can't create.

Fintech Brands with strong branding

B2B and B2C Dynamics Differ Dramatically

Fintech spans very different customer types:

B2C fintech (serving consumers):

Emotional purchase decisions

Trust built through experience and word of mouth

Brand personality can be more expressive

Social proof from users and reviews

Lower individual transaction value, higher volume

B2B fintech (serving businesses):

More rational evaluation process

Trust built through credentials and references

Brand must signal enterprise readiness

Social proof from customer logos and case studies

Higher individual value, longer sales cycles

Infrastructure fintech (serving other fintechs):

Technical evaluation primary

Developer experience is brand experience

Documentation and reliability are brand signals

Trust from who else uses you

Very long-term relationships

Each requires different brand approaches while maintaining coherent company identity.

The Trust Architecture

Every fintech brand needs a trust architecture — the systematic way you build and maintain customer confidence.

Layer 1: Foundational Trust

The baseline credibility required to even be considered:

Without foundational trust, nothing else matters. A beautiful brand on top of missing credentials is a house built on sand.

Layer 2: Social Proof

Evidence that others trust you:

Customer scale:

Number of users/customers

Transaction volume

Assets under management

Customer quality:

Recognizable logos (B2B)

User testimonials

Case studies with results

Third-party validation:

Press coverage

Industry awards

Analyst recognition

App store ratings

Community:

User communities

Social media following

Customer advocacy

Layer 3: Experience Trust

Trust built through direct interaction:

Product experience:

Reliability (uptime, performance)

Usability (intuitive, clear)

Transparency (fees, terms, status)

Communication experience:

Clear, honest messaging

Responsive support

Proactive problem acknowledgment

Design experience:

Professional, polished visual design

Consistent brand across touchpoints

Attention to detail signals care

Layer 4: Relationship Trust

Trust deepened over time:

Consistency:

Delivering on promises repeatedly

Stable, reliable service

Predictable communication

Responsiveness:

Quick support when needed

Acknowledgment of issues

Visible improvement over time

Advocacy:

Going beyond requirements

Customer education

Community support

Building Trust Over Time

Trust isn't built through marketing — it's built through experience. But brand creates the context for trust to develop:

Initial encounter: Brand creates first impression that opens door to considerationEarly experience: Product experience validates or contradicts brand promiseOngoing relationship: Consistent brand experience deepens trustCrisis moments: How brand handles problems determines long-term trustAdvocacy: Trusted brands earn customers who advocate for them

The strongest fintech brands think about trust at every stage, not just acquisition.

Visual Identity for Fintech

Fintech visual identity must balance innovation with stability, approachability with professionalism.

Color Strategy

Color in fintech carries significant weight:

Blue: The dominant financial services color. Signals trust, stability, security. Used by virtually every traditional bank and many fintechs. Safe but undifferentiated.

Recommendation: If you're early-stage and need maximum trust, blue or black is safest. If you're differentiated and targeting younger/digital-native audiences, bolder colors can work. The key is execution — any color can work with sufficient quality.

Typography Strategy

Typography in fintech signals personality and professionalism:

Geometric sans-serif: Clean, modern, tech-forward. The SaaS/fintech default.

Inter, SF Pro, Circular, Graphik

Signals: Modern, efficient, digital-native

Humanist sans-serif: Warmer, more approachable while remaining professional.

Source Sans, Open Sans, Lato

Signals: Approachable, friendly, human

Grotesque/Neo-grotesque: Character with professionalism. Distinctive without being decorative.

Helvetica, Akkurat, Grotesk varieties

Signals: Confident, established, quality

Serif (for contrast): Traditional authority. Can work for headlines or specific applications.

Editorial serifs for premium feel

Signals: Established, authoritative, premium

Custom typography: Maximum differentiation. Several leading fintechs have invested in custom type.

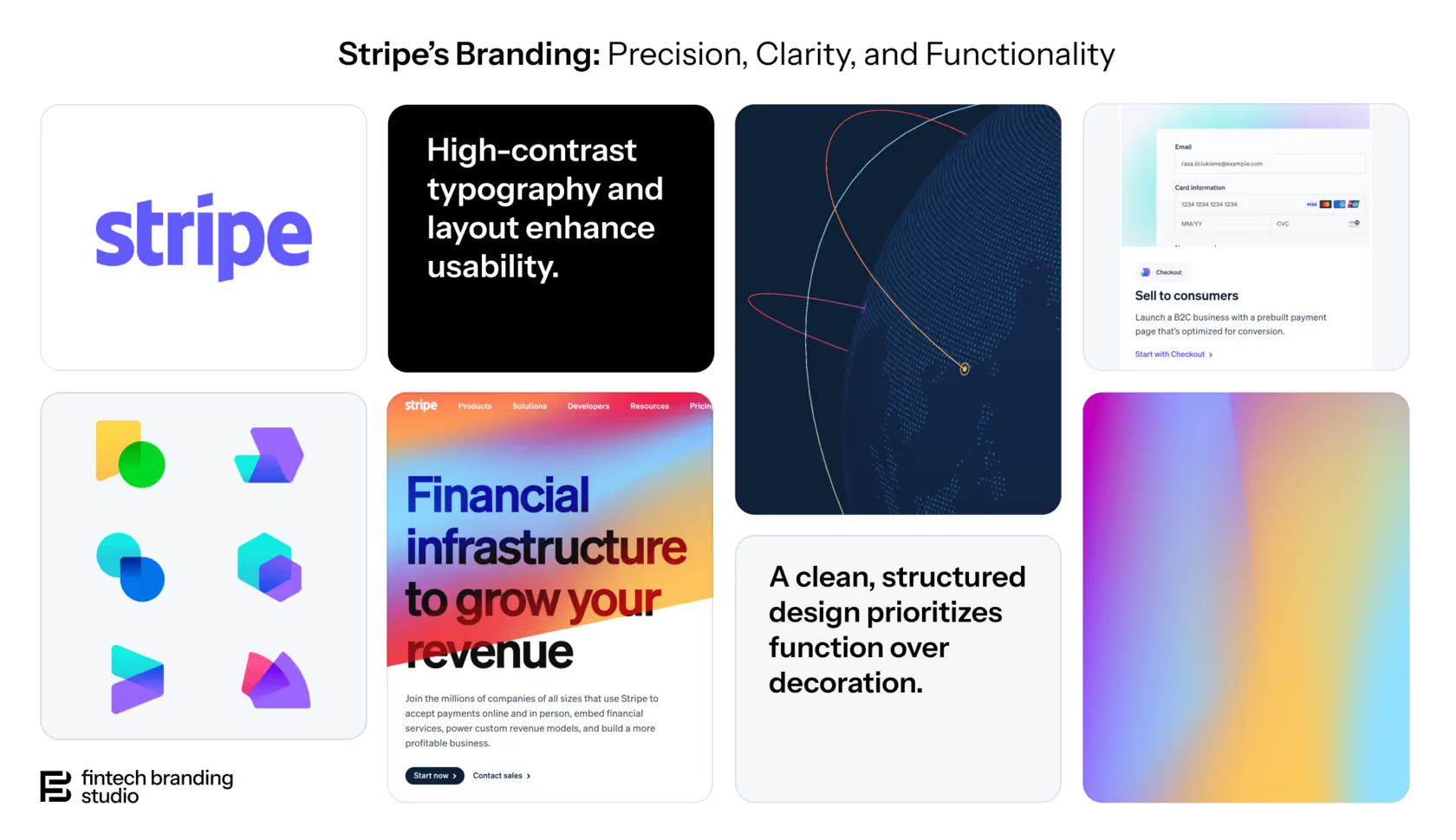

Stripe: Custom type contributes to distinctive identity

Signals: Investment, permanence, quality

Avoid: Decorative fonts, script fonts, novelty fonts. In finance, typography that draws attention to itself undermines trust.

Imagery and Illustration

Photography:

Real people (not obvious stock) build authenticity

Diverse representation matters

Avoid clichéd "person looking at phone smiling" shots

Environmental/lifestyle photography can work for consumer products

Professional headshots for B2B/enterprise

Illustration:

Can differentiate in a photography-heavy category

Must be professional quality — amateur illustration destroys trust

Abstract > literal for fintech (avoid money/coin clichés)

Consistent style across all applications

Product UI:

Screenshots build credibility (product exists)

Clean, professional UI is a trust signal

Mobile app screenshots especially important for consumer fintech

Dashboard screenshots for B2B

Data visualization:

Charts and graphs are natural for finance

Custom data viz style can differentiate

Clarity over decoration — must be readable

What to avoid:

Stacks of coins, flying money imagery (clichéd, cheap-looking)

Generic "business" stock photography

Overly playful illustration that undermines seriousness

Complex visual effects that distract from message

Logo Considerations

Fintech logos must work across many contexts:

App icon: Primary visibility for consumer fintech. Must be distinctive at small sizes, work on various backgrounds.

Card design: If you issue cards, logo appears on physical card. Simple marks work better than complex wordmarks.

Digital interfaces: Logo in app headers, emails, documents. Must scale down cleanly.

Co-branding: Partner integrations often show logos together. Needs to hold its own alongside other brands.

Print/Physical: Some fintech still has physical touchpoints — statements, cards, signage.

Logo types for fintech:

Wordmark: Works well when name is distinctive. Stripe, Plaid, Chime.

Symbol + wordmark: Flexibility for different contexts. Coinbase, Revolut.

Monogram/lettermark: Compact, works well as app icon. Square (symbol), Cash App.

Abstract mark: Distinctive but requires brand building. PayPal's overlapping Ps.

Design System Considerations

Fintech products are complex. Design systems must handle:

Data density: Financial interfaces show lots of numbers, tables, charts. Typography and spacing must support readability.

States and feedback: Loading, success, error, pending — financial products need clear state communication.

Accessibility: Financial services should be accessible to everyone. WCAG compliance is both ethical and often legally required.

White-labeling (B2B): If you power others' products, your design system may need to accommodate partner brands.

Wise Fintech Branding

Messaging for Fintech

Fintech messaging must communicate value while maintaining trust and satisfying compliance.

The Clarity Imperative

Financial products are often complex. Clear communication is a competitive advantage and a trust-builder.

Explain simply: Customers shouldn't need financial expertise to understand what you do.

Avoid jargon: "APY," "AUM," "settlement" — these mean nothing to most consumers. Translate or explain.

Be specific: Vague claims about "better" or "easier" don't build trust. Specific claims do.

Anticipate questions: What will people wonder? Answer proactively.

Siegel+Gale research found that 63% of consumers are willing to pay more for simpler experiences. In financial services, where complexity is the norm, simplicity is valuable.

Security and Trust Messaging

Communicate security without triggering anxiety:

State credentials matter-of-factly:

"256-bit encryption protects your data"

"FDIC insured up to $250,000"

"SOC 2 Type II certified"

Don't over-emphasize security: Constantly talking about security can backfire — it reminds people to worry. State it clearly, then move on.

Show, don't tell: A professional, polished experience communicates security better than claiming it.

Be transparent about what you're not:

If you're not a bank, say so clearly

If funds aren't FDIC insured, disclose it

Honesty about limitations builds trust

Value Proposition Messaging

What do customers get?

For consumer fintech:

Lead with benefit: "Banking that actually helps you save"

Support with features: "Round-ups, savings goals, no hidden fees"

Prove with evidence: "Members have saved an average of $1,200/year"

For B2B fintech:

Lead with outcome: "Accept payments anywhere, instantly"

Support with capability: "One integration, 135+ payment methods, 185 countries"

Prove with social proof: "Powering payments for Shopify, Instacart, and Lyft"

For infrastructure fintech:

Lead with capability: "Bank account connectivity for your app"

Support with technical proof: "11,000+ institutions, 99.9% uptime, bank-level security"

Prove with adoption: "Used by Venmo, Robinhood, and Coinbase"

Regulatory-Compliant Messaging

Working within regulatory constraints:

Partner with legal early: Don't write messaging in a vacuum. Legal review should happen before finalization, not after.

Build compliant templates: Create pre-approved language for common claims so teams can move fast within guardrails.

Disclosures as design challenge: Required disclosures don't have to be hidden fine print. Well-designed disclosure can build trust.

Country/jurisdiction awareness: Different rules in different places. Ensure messaging is appropriate for where it appears.

Claims to be careful with:

Return/performance claims (heavily regulated)

"Free" claims (must actually be free)

Comparisons to competitors (must be substantiated)

Guarantees (usually prohibited or heavily constrained)

Risk statements (often required, specific language mandated)

Tone of Voice

Fintech tone must balance multiple needs:

Trustworthy but not stuffy: Traditional bank communication is formal and cold. You can be warmer while remaining professional.

Confident but not arrogant: Financial services requires confidence — you're handling money. But arrogance undermines trust.

Simple but not simplistic: Clear communication doesn't mean dumbing down. Respect customer intelligence while making things accessible.

Empathetic but not patronizing: Financial decisions are emotional. Acknowledge this without condescending.

Helpful but not salesy: Hard selling doesn't work in finance. Education and guidance build trust.

Spectrum positions for typical fintech:

Formal ←—●—→ Casual: Slightly toward casual (more approachable than banks, but still professional)

By making infrastructure feel premium and developer-focused, Stripe differentiated from commoditized payment processing. The brand says "this is different, this is better" before you even see the product.

Revolut: Ambitious Scale

Revolut built a global fintech brand with aggressive positioning.

What they did:

"Super app" positioning: Positioned as comprehensive financial platform, not single product. Ambitious scope as differentiator.

Bold visual identity: Gradient, modern visual language. Distinctive in traditional banking context.

Global from start: Brand designed for international expansion. Works across markets.

Feature velocity: Constantly shipping new features. Brand communicates innovation and ambition.

Why it worked:

In markets with poor traditional banking (UK, Europe), aggressive challenger positioning resonated. The brand communicates "we're here to replace your bank" — ambitious but credible given product scope.

Nubank: Category Disruption

Nubank became Latin America's largest fintech by positioning against terrible incumbent banks.

What they did:

Purple as rebellion: Deliberately chose purple to contrast with traditional bank colors. Visual differentiation as statement.

Customer obsession: Built brand around customer experience. Net Promoter Scores became marketing message.

Transparency: Radical transparency about fees (or lack thereof). Direct contrast with banks known for hidden charges.

Digital-native: Fully digital experience in market where branches still dominated. Brand = modern.

Why it worked:

In Brazil, traditional banks were genuinely terrible — high fees, bad service, complex products. Nubank positioned directly against these pain points with visual and verbal identity that said "we're the opposite."

Chime: Banking for Everyone

Chime built a major US neobank brand focused on accessibility.

What they did:

Underbanked focus: Positioned for people poorly served by traditional banks. Not trying to steal Chase customers — serving people Chase doesn't want.

Simple, friendly brand: Approachable visual identity. Green as growth/money signal. Friendly illustration style.

Feature-led positioning: "No hidden fees," "Get paid early" — specific, valuable features as positioning.

Word of mouth: Built strong referral mechanics. Brand spread through communities.

Why it worked:

By focusing on underbanked customers, Chime found audience with genuine pain points and lower acquisition costs. Brand communicated "banking that's on your side" to people who felt traditional banks weren't.

Plaid: Invisible Infrastructure

Plaid built a valuable brand while being largely invisible to end users.

What they did:

Developer-focused: Like Stripe, focused on developers who would implement. Technical credibility as brand foundation.

Customer logos as proof: "Powers Venmo, Robinhood, Coinbase" — powerful social proof even though end users don't know Plaid.

Trust and security emphasis: Handling bank connections requires extreme trust. Security messaging is central.

Category definition: Defined and owned "financial data connectivity" as category.

Why it worked:

Plaid built brand with the audience that mattered (developers and fintech companies) rather than trying to build consumer awareness for infrastructure product. Customer logos did the trust-building work.

Building Your Fintech Brand

Wise Brand Transformation

Step 1: Establish Trust Foundation

Before brand expression, ensure credibility basics:

Regulatory compliance and licenses

Security certifications

Banking partnerships (if applicable)

Leadership team with relevant experience

Clear legal structure and disclosures

Without these, brand is building on sand.

Step 2: Define Your Position

Answer clearly:

Who are you for? (Be specific about audience)

What problem do you solve? (The real pain, not features)

Why are you different? (From incumbents and other fintechs)

What category do you compete in? (Or create)

Fintech positioning must address both rational needs (features, pricing) and emotional needs (trust, confidence, aspiration).

Differentiates from competitors (including traditional institutions)

Maintains professionalism that builds trust

Works across digital touchpoints (app, web, cards)

Scales to your ambition

Step 5: Build Messaging System

Create messaging that:

Explains clearly what you do and why it matters

Addresses different audiences (technical, business, consumer)

Satisfies regulatory requirements

Builds trust through specificity and transparency

Differentiates from alternatives

Work with legal from the start, not after.

Step 6: Extend to Product Experience

Ensure brand lives in product:

Visual design consistent with brand identity

Copy and microcopy in brand voice

Onboarding that delivers on brand promise

Support experience that reflects brand values

Communication (emails, notifications) in brand voice

In fintech, product experience is primary brand experience.

Step 7: Plan for Crisis

Fintech will face trust challenges — outages, security incidents, regulatory issues, market events. Prepare:

Communication protocols for incidents

Pre-approved messaging frameworks

Rapid response capabilities

Post-incident trust rebuilding plans

How you handle problems defines brand more than how you handle success.

Summary: Fintech Brand Principles

Trust is everything. Every brand decision should be evaluated through trust lens. Does this build confidence or undermine it?

Balance innovation and stability. Too innovative = risky. Too stable = why not use a bank? Navigate the tension.

Clarity differentiates. Financial services is confusing. Clear, simple communication is competitive advantage.

Compliance is opportunity. Regulatory requirements force transparency. Make that a brand strength.

Product is brand. Users interact with your product daily. Product experience is primary brand experience.

Prepare for crisis. Things will go wrong. How you handle them defines long-term brand.

Earn trust over time. Trust isn't built through marketing. It's built through consistent, reliable experience. Brand creates context for trust to develop.

Frequently Asked Questions

How do fintech startups build trust quickly?

Trust in fintech comes from layered signals. Foundational: regulatory licenses, security certifications (SOC 2, PCI DSS), banking partnerships, FDIC insurance where applicable. Social proof: customer count, recognizable logos, reviews and ratings, press coverage. Experience: professional design that signals competence, clear communication about terms and fees, responsive support. Relationship: consistent delivery on promises over time. No single element creates trust — it's the accumulation. Start with foundational signals (non-negotiable), then build social proof and experience.

Should fintech brands look more like tech companies or banks?

Neither extreme works. Looking too much like traditional banks (conservative, formal, blue) loses the differentiation that makes fintech compelling. Looking too much like consumer tech (playful, casual, colorful) can undermine trust with people's money. The sweet spot: professional enough to trust, modern enough to feel like a better alternative to banks. Study successful fintechs — Stripe balances premium with technical, Chime feels friendly but not frivolous, Revolut is bold but still credible. Let your audience guide calibration.

What regulatory constraints affect fintech branding?

Financial services marketing is heavily regulated. Constraints include: restrictions on performance claims (can't guarantee returns), required disclosures (APRs, fees, risks) that affect design and copy, rules about "free" claims (must actually be free), compliance review on all marketing materials, geographic limitations on what you can offer and say, and specific language required for certain products. Build legal review into your brand process from the start, not after. Create pre-approved messaging templates for common claims. Treat compliance as brand opportunity — clear, transparent communication differentiates from murky incumbent practices.

Build Your Fintech Brand

If you're building a fintech company and need brand that builds trust, differentiates from competitors, and satisfies regulatory requirements — we can help.

Metabrand specializes in branding for fintech and financial services. We understand the unique dynamics — trust requirements, regulatory constraints, technical complexity — and build brands that work in this demanding environment.